PRMIA 8008 - PRM Certification - Exam III: Risk Management Frameworks, Operational Risk, Credit Risk, Counterparty Risk, Market Risk, ALM, FTP - 2015 Edition

Which of the following statements are true:

I. Common scenarios for stress tests include the 1997 Asian crisis, the Russian default in 1998 and other well known economic stress situations.

II. Stress tests provide the assurance that an institution's worst case losses will be covered.

III. Performing stress tests is highly recommended but is not mandated under Basel II.

IV. Historical events can be modeled quite accurately as they have defined start and end dates.

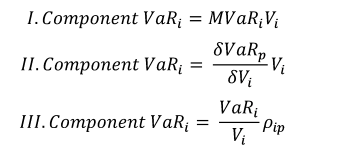

Which of the following formulae correctly describes Component VaR. (p refers to the portfolio, and i is the i-th constituent of the portfolio. MVaR means Marginal VaR, and other symbols have their usual meanings.)

A long position in a credit sensitive bond can be synthetically replicated using:

Which of the following statements is true:

I. When averaging quantiles of two Pareto distributions, the quantiles of the averaged models are equal to the geometric average of the quantiles of the original models based upon the number of data items in each original model.

II. When modeling severity distributions, we can only use distributions which have fewer parameters than the number of datapoints we are modeling from.

III. If an internal loss data based model covers the same risks as a scenario based model, they can can be combined using the weighted average of their parameters.

IV If an internal loss model and a scenario based model address different risks, the models can be combined by taking their sums.

Which of the following cannot be used as an internal credit rating model to assess an individual borrower:

For identical mean and variance, which of the following distribution assumptions will provide a higher estimate of VaR at a high level of confidence?

In the case of historical volatility weighted VaR, a higher current volatility when compared to historical volatility:

The diversification effect is responsible for:

When doing stress tests based on historical scenarios, if no appropriate historical scenarios exist for a security, it is most INAPPROPRIATE to:

Which of the following statements is NOT true in relation to the recent financial crisis of 2007-08?