PRMIA 8010 - Operational Risk Manager (ORM) Exam

If a borrower has a default probability of 12% over one year, what is the probability of default over a month?

What would be the consequences of a model of economic risk capital calculation that weighs all loans equallyregardless of the credit rating of the counterparty?

I. Create an incentive to lend to the riskiest borrowers

II. Create an incentive to lend to the safest borrowers

III. Overstate economic capital requirements

IV. Understate economic capitalrequirements

The unexpected loss for a credit portfolio at a given VaR estimate is definedas:

If the cumulative default probabilities of default for years 1 and 2 for a portfolio of credit risky assets is 5% and 15% respectively, what is the marginal probability of default in year 2 alone?

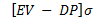

If EV be the expected value of a firm's assets in a year, and DP be the 'default point' per the KMV approach to credit risk, and σ be the standard deviation of future asset returns, then the distance-to-default is given by:

A)

B)

C)

D)

Which loss event type is the loss of personally identifiableclient information classified as under the Basel II framework?

All else remaining the same, an increase in the joint probability of default between two obligors causes the default correlation between the two to:

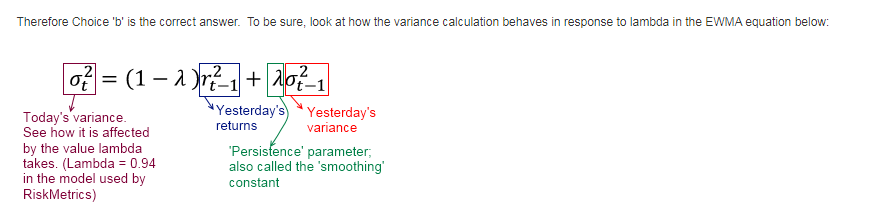

As the persistence parameter under EWMA is lowered, which of the following would be true:

According to the implied capital model, operational risk capital is estimated as:

In estimating credit exposure for a line of credit, it is usual to consider: