CIMA BA2 - Fundamentals of management accounting

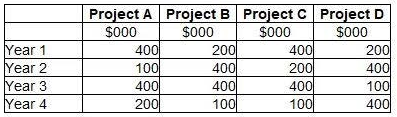

A company is appraising two projects. Both projects are for five years. Details of the two projects are as follows.

Based on the above information, which of the following statements is correct?

Which TWO of the following are characteristics of Management Accounts? (Choose two.)

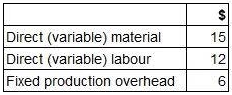

The forecast costs per unit for a new product are as follows:

The company uses marginal cost plus pricing and all products are required to achieve a 40% margin.

What would be the selling price per unit?

A company operates an integrated standard cost accounting system. The standard price of raw material A is $20 per litre. At the start of period 1, the inventory of 500 litres of raw material A was valued at $20 per litre. During period 1, 100 litres of raw material A were purchased at an actual price of $21 per litre. During period 2, 550 litres of raw material A were issued to Job 789.

In respect of the above events, which TWO of the following statements are correct? (Choose two.)

The year-to-date results at the end of month 9 included sales revenue of $3,600,000 and variable costs of $2,100,000.

During month 10, sales revenue was $450,000 and variable costs were $270,000.

What year-to-date contribution to sales ratio (C/S ratio) would be reported at the end of month 10?

Which of the following statements relating to risk and uncertainty is correct?

The concept of the time value of money:

A management accountant has forecast the following cash inflows from four potential projects.

All four projects require the same initial investment and will last for four years. They all result in a positive net present value but only one of the projects can be undertaken.

Which project should be selected?

Zelts Ltd earns a contribution of 20% of the selling price for product 'Y'. The annual fixed costs are £200,000.

In order to earn an annual profit of £100,000 the sales revenue needs to be:

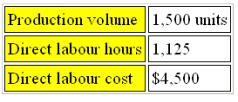

Refer to the exhibit.

The budget for ORG for the month of September contained the following data:

During the month the actual number of units produced was 1,550. The management accounts showed a direct labour rate variance of $200 adverse and direct labour efficiency of $150 adverse.

The actual direct labour cost in the month was: