CIMA F2 - F2 Advanced Financial Reporting

The yield to maturity of a redeemable bond is calculated as the internal rate of return of the relevant cash flows associated with the bond.Â

Which TWO of the following are considered relevant cash flows in this calculation?

ST acquired 70% of the equity shares of DE for $87,500 on 30 September 20X5. At the date of acquisition the net assets of DE were $54,700 and the fair value of the non controlling interest was measured at $19,700. There has been no impairment of goodwill.

On 30 September 20X9 ST disposed of its entire investment in DE for $262,500 when the net assets of DE were $96,250.

What is the gain or loss on disposal of DE that will be included in ST's consolidated profit or loss for the year ended 30 September 20X9?

Which of the following, in accordance with IFRS 2 Share-based Payments, are only applicable to the accounting treatment of cash settled rather than equity settled share-based payment schemes?

Select ALL that apply.

Company A are approached by a wealthy and internationally famous investor shortly before the launch date of their IPO. He tells them that the company do not need to incur all of the cost and risk of an IPO, as he will

give them S55 million for 65% equity in the company.

Which of the following statements are also true of the offer? Select ALL that apply.

Which THREE of the following statements are true in relation to financial assets designated as fair value through profit or loss under IAS 39 Financial Instruments: Recognition and Measurement?

Which of the following reduce the usefulness of ratio analysis when comparing entities that operate in the same industry?

Select ALL that apply.

JJ's current share price is $1.80, with a dividend of $0.20 a share just about to be paid.

Dividends have increased at an average annual growth rate of 4.5% and this is expected to continue into the future.

What is JJ's cost of equity?

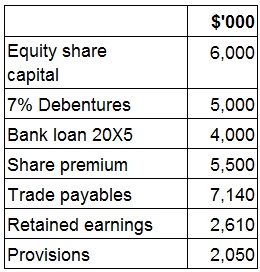

The following is extracted from MN's statement of financial position at 30 September 20X1.

Calculate the gearing (measured as debt:equity) ratio of MN at 30 September 20X1.

Give your answer to one decimal place.

%

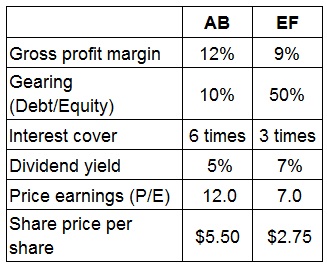

AB and EF are located in the same country and prepare their financial statements to 31 October in accordance with International Accounting Standards. EF supplies AB with a component that is vital to AB's product range. AB is considering acquiring a controlling interest in EF by 31 December 20X4 in order to guarantee future supply. The Board of EF has indicated that such an approach would be postively considered. AB would use its control to make AB the sole customer of EF.

The Finance Director of AB has been granted access to EF's management accounts and has conducted some initial analysis from the financial press. The results togther with comparisons for AB for the year to 31 October 20X4 are presented below:

AB and EF are forecasting revenues of S1,500,000 and $700,000 respectively for the year ended 31 October 20X5.

AB's Finance Director met with one of the directors of EF to discuss the potential impact of the acquisition.

Which of the director's statements below is correct?

An entity undertakes an issue of new debt which has the effect of reducing the entity's weighted average cost of capital (WACC).

Which of the following would best explain why the WACC will have fallen?