CIMA F2 - F2 Advanced Financial Reporting

LM acquired an asset under a 5-year non-cancellable operating lease agreement on 1 January 20X8. Under the terms of the agreement, LM paid nothing for the first year and then made four payments of $50,000 in each subsequent year.  LM adopted the provisions of IAS 17 Leases when accounting for this agreement.

Which of the following is correct in respect of this operating lease in LM's financial statements for the year to 31Â December 20X8?

If you were asked to express the overall performance of an entity as a percentage of its total investment in net assets which of the following ratios would you calculate?

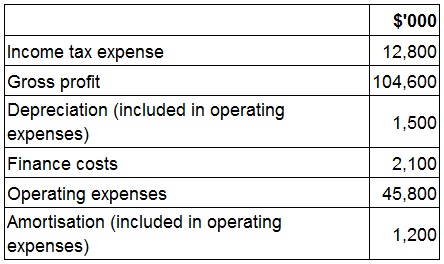

In recent years EBITDA has been adopted by large entities as a key measure of performance. The following figures have been extracted from the financial statements of UV for the year ended 30 November 20X9:

What is EBITDA for UV for the year ended 30 November 20X9?

Give your answer to the nearest $'000.

DE acquired 10% of the equity shares of KL on 31 December 20X2.

A further 50% of the equity shares of KL were acquired by DE on 1 January 20X4.

Which THREE of the following would be part of the process for recording the second purchase of shares?

VW acquired 240,000 of the 300,000 $1 equity shares of EF for $1,440,000 on 1 January 20X2. Goodwill arising from the acquisition, using the proportionate method for measuring non controlling interest, was $540,000. On 1 January 20X3 VW disposed of 30,000 of the equity shares in EF for $200,000 cash when the net assets of EF were £1,200,000. Goodwill arising on the acquisition of EF had not suffered any impairment.

Prepare the accounting adjustment that will be processed by VW to reflect the disposal of shares in EF when it prepares its consoldiated financial statements.

ST granted 1,000 share appreciation rights (SARs) to its 100 employees on 1 December 20X7. To be eligible, employees must remain employed for 3 years from the grant date. In the year to 30 November 20X8, 10 staff left and a further 20 were expected to leave over the following two years. The fair value of each SAR was $12 at 1 December 20X7 and $15 at 30 November 20X8.

What is the accounting entry to record this transaction for the year to 30 November 20X8?Â

MS Group's total profit for period on their consolidated income statement is £31,000. This includes adjusting for their share of joint venture JV2. Calculate the share of joint venture MS Group received based on the

following information.

MS operating profit £41,000

Dividend from JV2 £5,000

Finance cost £3,000

Tax £11,000

Which THREE of the following actions should improve the cash position of an entity?

Which of the following statements about ST is true?

You are a Financial Controller at BCD and are in the process of preparing the year-end financial statements. A member of your finance team has come to see you about her provisions balance at year-end.

She says that the Managing Director has asked her to increase the provisions balance by $1 million overall. She thinks this is because BCD has had a very good year in terms of profit, and the Managing Director wants to put some profit aside to protect against any future reductions in profit. $1 million is material to BCD.

You believe that the provisions balance was fairly stated without the additional $1 million.

Which TWO of the following would be appropriate actions in this scenario?