CIMA F3 - Financial Strategy

A young, capital intensive company has a large amount of tangible assets.

Intangibles, including brand name, are considered to be of negligible value at this time

Relevant data:

• The company operates a residual dividend policy.

• The industry in which the company operates is suffering from a large amount of uncertainty at present. Forecasting the future earnings or cashflows of the company is therefore extremely difficult

• There are very few quoted companies in the industry that are similar in size or in precisely the same business sectors.

Which method of valuation would be most suitable for this company?

A company is considering a divestment via either a management buyout (MBO) or sale to a private equity purchaser. Which of the following is an argument in favour of the MBO from the viewpoint of the original company?

Which THREE of the following remain unchanged over the life of a 10 year fixed rate bond?

Company A plans to acquire Company B, an unlisted company which has been in business for 3 years.

It has incurred losses in its first 3 years but is expected to become highly profitable in the near future.

No listed companies in the country operate the same business field as Company B, a unique new high-risk business process.

The future success of the process and hence the future growth rate in earnings and dividends is difficult to determine.

Company A is assessing the validity of using the dividend growth method to value Company B.

Which THREE of the following are weaknesses of using the dividend growth model to value an unlisted company such as Company HHG?

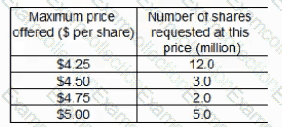

Company C invests heavily in Research and Development an need to raise $45 million to finance future projects. It has decided to use equity finance raised by a tender offer, The following tender offers have been received from potential investors:

Company C wishes to select an offer price that will project shareholders from a significant dilution of control but still raise the required amount of finance.

What offer price should Company C’s select?

A company is planning a share buyback. In which of the following circumstances would a share buyback be appropriate?

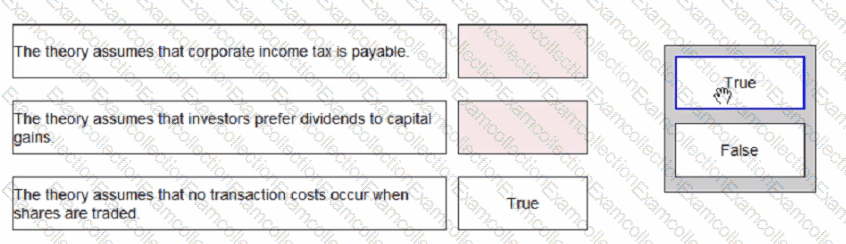

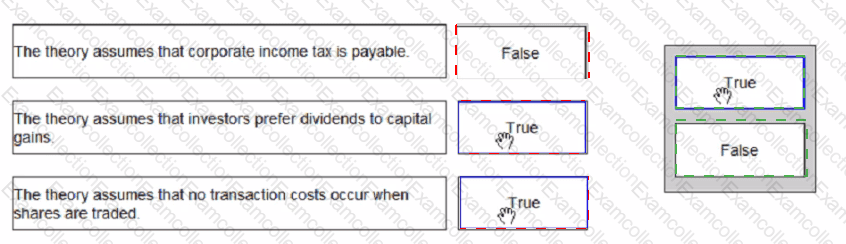

Select whether the following statements are true or false with regard to Modigliani and Miller's dividend policy theory.

Two listed companies in the same industry are joining together through a merger.

Â

What are the likely outcomes that will occur after the merger has happened?Â

Select ALL that apply.

An entity prepares financial statements to 30 June.

During the year ended 30 June 20X2 the following events occurred:

Â

1 July 20X1

• The entitiy borrowed $100 million at a variable rate of interest.

• In order to protect itself against the variability of its interest cashflows, the entity entered into a pay-fixed-receive-variable interest swap with annual settlements. The fair value of the swap on this date was zero.

30 June 20X2

• The entity received a net settlement of $2 million under the swap. After this net settlement, the fair value of the swap was $5 million - a financial asset.

The entity decides to use hedge accounting for this arrangement and has designated it as a cash flow hedge. The swap is a perfect hedge of the variability of the cash interest payments.

Â

Which of the following describes the treatment of the settlement and the change in the fair value of the swap in the statement of profit or loss and other comprehensive income for the year ended 30 June 20X2?