CIMA P2 - Advanced Management Accounting

The net present value of the cost of operating a machine for the next 4 years is £6,340. The discount rate used is 10%.

What is the equivalent annual cost and the present value of the cost in perpetuity of operating this machine?

Use discount factors to 3 decimal places.

A risk averse decision maker will:

An organization wishes to achieve cost reductions for a product it already has in production without affecting the customer's perception of the product.

It has decided to carry out a systematic examination of the factors affecting the cost of the product in order to identify ways of achieving the specified purpose at lower cost while maintaining the required standard and quality.

Which of the following correctly identifies the activity that the organization is undertaking?

A public sector service organization is considering whether to use a balanced scorecard or a value for money approach based on the three Es to assess its performance.

Which of the following are correct comparisons of the balanced scorecard and value for money based on the three Es as performance measurement frameworks?

Select ALL that apply.

The starting point for developing a balanced scorecard for an organization should be:

A company is comprised of two divisions, each of which manufactures a single product. Division A manufactures a product which can be sold in a perfect external market or transferred as an intermediate product to division B. Division B finishes the intermediate product and sells this in a perfect external market.

Due to company policy, internal transfers are recorded at the external market price. At this transfer price both divisions make a profit from their activities.

Which of the following will NOT be achieved by the company's transfer pricing policy?

A manager must decide which one of three projects should be implemented. For each project the possible outcomes and their associated probabilities can be estimated reliably. The manager has decided to make the decision based solely on which project has the highest expected value of profit.

Which of the following statements are correct?

Select ALL that apply.

A manufacturing company has just developed a new product and must now determine the most appropriate pricing strategy for its initial launch.

The product will initially be unique because it will include highly desirable features that no competitive product offers. Its development has involved substantial expenditure and the company wishes to recover this as soon as possible.

The product's uniqueness is expected to last for only six months before a competitor launches a similar product. It is expected that the competitor will avoid any significant development costs by reverse engineering the company's own product.

At that point, to remain competitive, the company must ensure that its selling price matches that of the competitor.

Which of the following pricing strategies would be most suitable for the initial launch of the company's product?

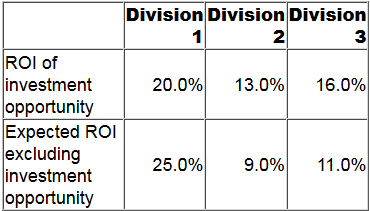

A company has three divisions, each of which is an investment centre. The divisional managers' performance is assessed using return on investment (ROI). A higher ROI will result in a higher bonus for the divisional manager.

The company's cost of capital is 15%.

For the forthcoming year each divisional manager has one investment opportunity available as follows:

The manager(s) of which division(s) will proceed with their respective investment opportunity?

An investment centre manager is considering the purchase of a new machine. If purchased, the new machine would replace an existing one that is used to manufacture one of the investment centre's existing products.

The new machine would incur $800 per month additional running costs; this includes $300 per month of additional depreciation.

The new machine would save on direct labor time. This means that the fixed production overhead absorbed by the product on the basis of direct labor hours would reduce by $100 per month.

What is the total cost of the above that is relevant to the decision to purchase the machine?