PRMIA 8010 - Operational Risk Manager (ORM) Exam

When combining separate bottom up estimates of market, credit and operational risk measures, a most conservative economic capital estimate results from which of the following assumptions:

Which of the following statements are true ?

I.Risk governance structures distribute rights and responsibilities among stakeholders in the corporation

II. Cybernetics is the multidisciplinary study of cyber risk and control systems underlying information systems in an organization

III. Corporate governance is a subset of the larger subject of risk governance

IV. The Cadbury report was issued in the early 90s and was one of the early frameworks for corporate governance

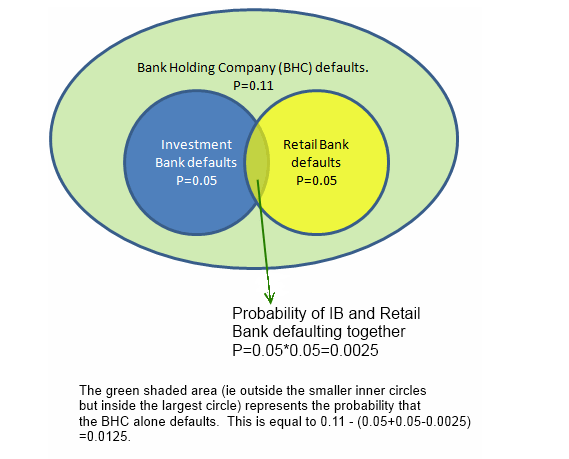

A Bank Holding Company (BHC) is invested in an investment bank and a retail bank. The BHC defaults for certain if either the investment bank or the retail bank defaults. However, the BHC can also default on its own without either the investment bank or the retail bank defaulting. The investment bank and the retail bank's defaults are independent of each other, with a probability of default of 0.05 each. The BHC's probability of default is 0.11.

What is the probabilityof default of both the BHC and the investment bank? What is the probability of the BHC's default provided both the investment bank and the retail bank survive?

The CDS quote for the bonds of Bank X is 200 bps. Assuming a recovery rate of 40%, calculate the default hazard rate priced in the CDS quote.

Which of the following is not true about the ISDA master agreement (ISDA MA):

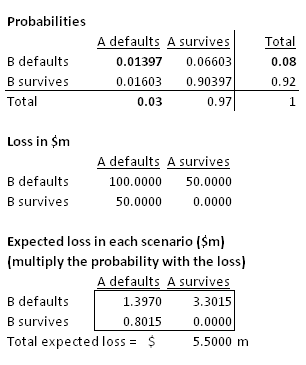

There are two bonds in a portfolio, each with a market value of $50m. The probability of default of the two bonds are 0.03 and 0.08 respectively, over a one year horizon. If the default correlation is 25%, what is the one year expected loss on this portfolio?

Concentration risk in a creditportfolio arises due to:

A loan portfolio's full notional value is $100, and its value in a worst case scenario at the 99% level of confidence is $65. Expected losses on the portfolio are estimated at 10%. What is the level of economic capital required to cushion unexpected losses?

Which of the following are valid criticisms of value at risk:

I. There are many risks that a VaR framework cannot model

II. VaR does not considerliquidity risk

III. VaR does not account for historical market movements

IV. VaR does not consider the risk of contagion

For a corporate bond, which of the following statements is true:

I. The credit spread is equal to the default rate times the recovery rate

II. The spread widens when the ratings of the corporate experience an upgrade

III. Both recovery rates and probabilities of default are related to the business cycle and move in oppositedirections to each other

IV. Corporate bond spreads are affected by both the risk of default and the liquidity of the particular issue