PRMIA 8010 - Operational Risk Manager (ORM) Exam

An error by a third party service provider results in a loss to a client that the bank has to make up. Such as loss would be categorized per Basel IIoperational risk categories as:

A risk analyst peforming PCA wishes to explain80% of the variance. The first orthogonal factor has a volatility of 100, and the second 40, and the third 30. Assume there are no other factors. Which of the factors will be included in the final analysis?

Which of the following decisions need to be made as part of laying down a system for calculating VaR:

I. How returns are calculated, eg absoluted returns, log returns or relative/percentage returns

II. Whether VaR is calculated based on historical simulation, Monte Carlo, or is computed parametrically

III. Whether binary/digital options are included in the portfolio positions

IV. How volatility is estimated

Under thebasic indicator approach to determining operational risk capital, operational risk capital is equal to:

The VaR of a portfolio at the 99% confidence level is $250,000 when mean return is assumed to be zero. If the assumption of zero returns is changed to an assumption of returns of $10,000, what is the revised VaR?

Under the standardized approach to determining operational risk capital, operations risk capital is equal to:

Aderivative contract has a negative current replacement value. Which of the following statements is true about its loan equivalent value for credit risk calculations over a 2-year horizon?

The frequency distribution for operational risk loss events can be modeled by which of the following distributions:

I. The binomial distribution

II. The Poisson distribution

III. The negative binomial distribution

IV. The omega distribution

Credit exposure for derivatives is measured using

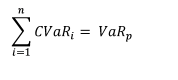

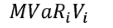

Which of the formulae below describes incremental VaR where a new position 'm' is added to the portfolio? (where p is theportfolio, and V_i is the value of the i-th asset in the portfolio. All other notation and symbols have their usual meaning.)

A)

B)

C)

D)