CIMA BA3 - Fundamentals of financial accounting

The valuation of inventory in a manufacturing company will consist of:

Which one of the following book-keeping errors does not affect the view given by the financial accounts?

Different users have different needs from financial information. One of which is to know about the company's ability pay its debts

Which of the following users will have this need for information?

Which one of the following would not contribute to the prevention and detection of fraud?

Which of the following is the correct double entry for a prepayment?

Refer to the exhibit.

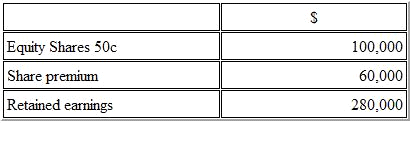

A company has the following equity balances at the beginning of the year

During the year the company made a rights issue of 1 for 5 at a price of $1.50

The balance of share premium after this issue is

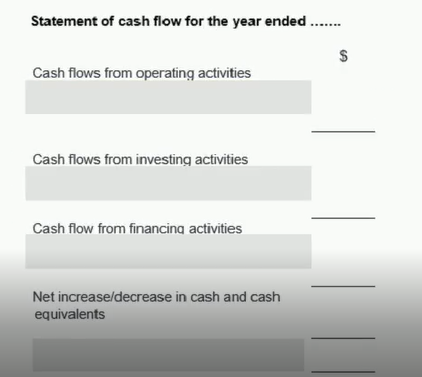

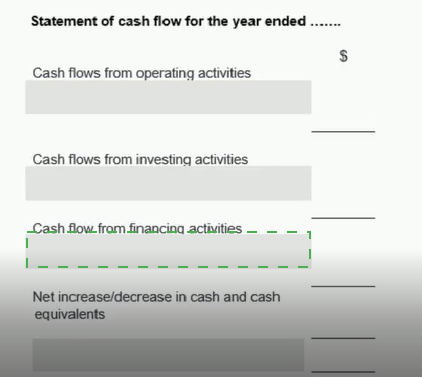

In which section of the statement of cash flow would cash from share issues be included? Select one of the following

Statement of cash How for the year ended.......

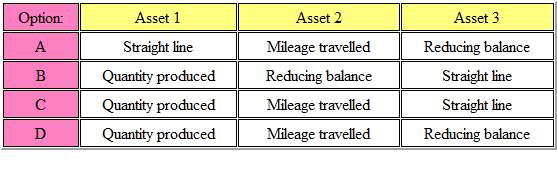

Refer to the Exhibit.

A business has three non-current assets.

(i) Asset 1 will be used to manufacture components over a 4 year period, after which it will be scrapped; the total contract is for 1 million components, to be produced in different quantities each year.

(ii) Asset 2 is a motor car for a director; it is expected to be kept for 3 years, and will travel 20,000 miles each year.

(iii) Asset 3 is a mobile truck used for transporting goods around the factory; it is expected to be kept for 20 years.

Which one of the following combinations of depreciation methods, would be most reasonable for the above three assets?

The answer is:

Which of the following are possible reason for a credit balance on the sales ledger account of a customer?

(a) A contra entry between the sales ledger and the purchase ledger has been carried out for an amount in excess of the sales ledger balance

(b) A customer has returned goods subsequent to making payment for them

(c) A credit note has been issued in error

(d) A bad debt written off has subsequently been paid

Your company provides a number of staff with lap-top computers, as well as pocket calculators. It capitalizes the cost of the computers and depreciates them over several years, but writes off the cost of the pocket calculators in full, against profits, in the period in which they are purchased.

The main justification for this difference in treatment is: