CIMA BA3 - Fundamentals of financial accounting

The profit earned by Subramanian in 2006 was £ 50,000. He injected new capital of £12,000 during the year and withdrew goods for his private use that cost £4,000.

If net assets at the beginning of 2006 were £10,000, what were the closing net assets?

Your organization owed VAT of $22,700 at the beginning of the month.

During the month, it sold standard-rated goods with a net value of $600,000. Its purchases and expenses during the same month amounted to $188,000 including VAT. It paid VAT to the Revenue and Customs, of $33,400. The VAT rate is 17.5%

At the end of the month, the balance on the VAT account was:

A company had a gross profit margin of 40%. Sales for the period were $280,000 and opening and closing inventories were $18,000 and $16,000 respectively.

Purchases for the period were therefore

Financial controls are needed in order to:

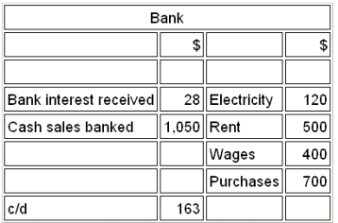

Refer to the Exhibit.

Which of the following would be the opening balance on the bank ledger account?

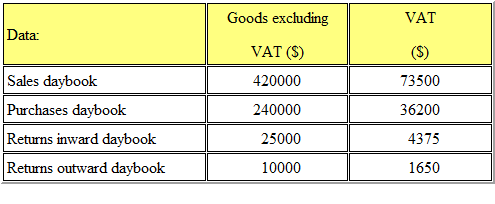

Refer to the Exhibit.

The following totals appear in a company's daybooks for the month of May. VAT is recoverable on all purchases which were in respect of goods for resale.

Opening inventory was £350,00 and closing inventory was $37,500.

The gross profit for the period was

An organization's trial balance at the end of the month was out of agreement, with the debit side totaling £500 less than the credit side. A suspense account was opened for this amount.

During the next month, the following errors were discovered:

(a) The purchase returns day book had been under cast by £50

(b) Rent payable of £400 had been credited to the rent receivable account

(c) A non-current asset, with a net book value of £700 had been disposed of at a loss of £80; all entries had been correctly recorded except that the sale proceeds had been omitted from the disposals account.

Following the correction of these errors, the balance on the suspense account would be.

Who is responsible for ensuring that internal control systems operate efficiently?

MHJ purchased an asset for £53,500, which incurred a delivery charge of £20,000. MHJ decided to set a depreciation rate of 15% per annum for the asset.

In its second year, the asset is re-valued at 180% of the net carrying value of the previous year.

What will be the asset's net carrying amount by the end of its second year?

The suspense account of a company was opened with a credit balance of $360 when the trial balance failed to agree.

This could have arisen because