CIMA F1 - Financial Reporting

The following information relates to AA.

Extract of Trial Balance at 31 December 20X4;

Notes

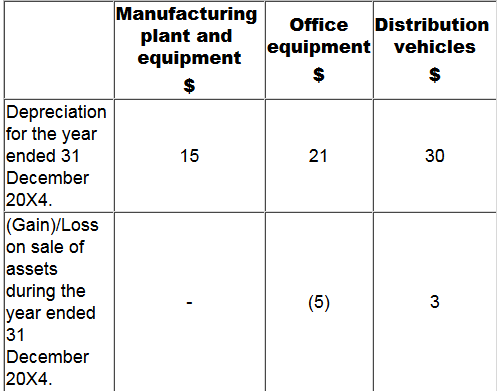

(i) Inventory at 31 December 20X4 was valued at cost at $30.

(ii) The loan which was received on 1 July 20X4 is repayable in 20X9.

(iii) Corporate income tax represents an over-provision of tax for the year ended 31 December 20X3. AA reported a loss for tax purposes for the year ended 31 December 20X4 and a tax refund is expected amounting to $20.

(iv) Cost of sales, administration and distribution costs need to be adjusted for the following:

Calculate gross profit for the year ended 31 December 20X4.

Give your answer as a whole $.

PP supplies zero-rated and standard-rated goods. During the year ended 30 March 20X3, the standard-rated goods made up 50% of the total supplies. During the year ended 30 March 20X4 this percentage increased to 60%.

What percentage of input tax suffered can PP claim back in the year ended 30 March 20X4?

Give your answer as a whole number.

The International Accounting Standards Board's "The Conceptual Framework for Financial Reporting" (known as The Conceptual Framework) states that "faithful representation" is a fundamental qualitative characteristic.

In accordance with the Conceptual Framework which of the following is NOT part of faithful representation?

Which TWO of the following are functions of the International Financial Reporting Standards (IFRS) Advisory Council?

EFG purchased an asset on 1 January 20X5 for $24,000. On that date its useful life was 5 years and residual value was expected to be nil. EFG calculates depreciation on a pro-rata basis.

The asset is reclassified as held for sale on 1 October 20X8 and is unsold on 31 December 20X8.

It is expected that the asset will be sold for S6;300 and that selling costs will be S500

What is the amount that this asset will be included at in EFG's statement of financial position at 31 December 20X8?

Give your answer to the nearest $.

Which of the following does the phrase 'events after the reporting period' refer to?

An entity purchased equipment on 1 April 20X4 for $200,000. The equipment was depreciated using the reducing balance method at 20% a year.

Depreciation was charged up to and including 31 March 20X7. At that date the recoverable amount of the equipment was $94,000.

Calculate the impairment loss on the equipment in accordance with IAS 36 Impairment of Assets.

Give your answer to the nearest whole $.

While conducting their audit, auditor 0 did not encounter issues which significantly limited the scope of their audit, however they did run into problems in that they disagreed with the management on facts in the

statements.

These disagreements were somewhat material, but they did not affect the auditor's overall opinion of the business. Which of the following statements should auditor 0 issue?

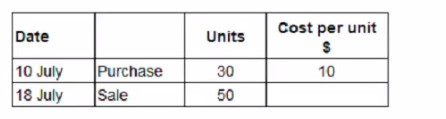

On 1 July 20X8 JKL has 100 units of inventory, which cost $8 each. The following transactions arose during the month of July:

JKL values inventory using the first in. first out method.

What is the value of JKL's inventory at 31 July 20X8?

Give your answer to the nearest $.

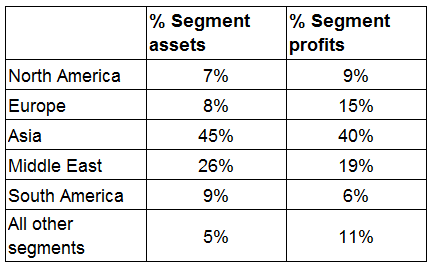

OP has five main geographic segments and reports segmental information in accordance with IFRS 8 Operating Segments.

Which THREE of the following would be regarded as operating segments of OP in accordance with IFRS 8?