CIMA F1 - Financial Reporting

Country X charges corporate income tax at the rate of 20% on all income irrespective of whether it is paid out as a dividend. Country Y charges corporate income tax at the rate of 25% on all income.

An entity, AA, which is resident in Country X pays a dividend of $100,000 to another entity, BB, which is resident in Country Y.

Countries X and Y have a double taxation treaty which adopts the exemption method in respect of this type of transaction.

What is BB's liability to tax in Country Y in respect of the dividend income received?

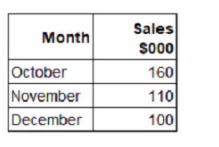

XYZ has the following data relating to the forecast sale of goods for the quarter to 31 December 20X2:

XYZ expects trade receivables to be settled as follows:

• 20% in the month of sale, by offering a settlement discount of 5%;

• 30% in the month following sale, and

• the remainder, after allowing for irrecoverable debts, in the subsequent month

$10,000 of the sales made in October 20X2 are expected to be irrecoverable

What is the forecast amount to be received by XYZ from trade receivables in December 20X2?

Which of the following are techniques that can be used by a company to ensure they receive timely payment of receivables? Select ALL that apply:

What does the exemption method of giving double taxation relief mean?

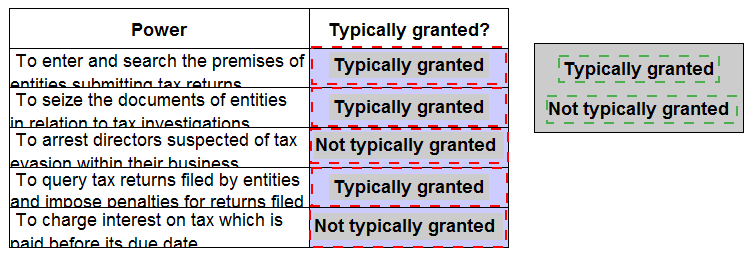

Identify which of the following are powers that a government would typically grant it's tax authority by placing the appropriate response beside each power.

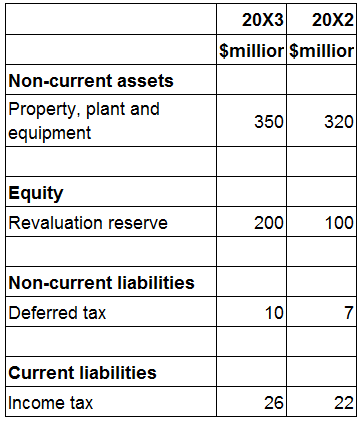

The following information is extracted from the statement of financial position for ZZ at 31 March 20X3:

Included within cost of sales in the statement of profit or loss for the year ended 31 March 20X3 is $20 million relating to the loss on the sale of plant and equipment which had cost $100 million in June 20X1.

Depreciation is charged on all plant and equipment at 25% on a straight line basis with a full year's depreciation charged in the year of acquisition and none in the year of sale.

The revaluation reserve relates to the revaluation of ZZ's property.

The total depreciation charge for property, plant and equipment in ZZ's statement of profit of loss for the year ended 31 March 20X3 is $80 million.

The corporate income tax expense in ZZ's statement of profit or loss for year ended 31 March 20X3 is $28 million.

ZZ is preparing its statement of cash flows for the year ended 31 March 20X3.

What figure should be included within cash flows from investing activities for the proceeds of sale of plant and equipment?

Which of the following is a feature of value added tax (VAT)?

An entity bought a capital item for $110,000 on 1 March 20X4 incurring legal fees at the date of purchase of $2,500.

On 1 May 20X4 additional costs classified as capital expenditure by the tax rules of the country of $25,000 were incurred in respect of the asset. On 1 June 20X4 repairs not classified as capital expenditure were incurred at a cost of $15,000.

The asset was sold for $250,000 on 30 November 20X8 and costs to sell were incurred of $4,300.

Calculate the chargeable gain on the disposal.

Give your answer to the nearest $.

STU commenced trading on 1 January. Total sales for the month of January were $250,000. which were 75% on credit and 25% for cash. Sales are expected to increase by 10% a month Irrecoverable debts are estimated to be 5% of credit sales Of the credit sales expected to pay, 50% pay in the month following the sale and the remaining 50% the month after.

The cash expected to be received in February is:

Which of the following would be the most immediate impact of overtrading?