CIMA F2 - F2 Advanced Financial Reporting

Which of the following statements are true regarding consolidated cash flows after the acquisition of a subsidiary?

Select ALL that apply.

RS has issued an instrument with a nominal value of $1 million, at a discount of 2.5%, and a coupon rate of 6%. The terms of the issue are that the instrument must either be redeemed at par, at the option of the holder, in three years' time, or alternatively converted into equity shares in RS.

The characteristics of this instrument taken as a whole indicates that it would be classifed as which of the following?

EF have just paid a dividend of 20 cents a share and the current share price is $3.75. EF regularly reinvests 40% of its profit for the year and generates a return on reinvested funds of 12%.

The cost of equity for EF using the dividend valuation model is:

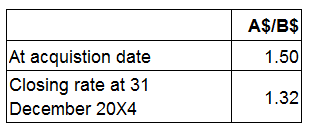

A group presents its financial statements in A$.

The goodwill of its only foreign subsidiary was measured at B$100,000 at acquisition. There have been no impairments to this goodwill.

Exchange rates (where A$/B$ is the number of B$'s to each A$) are as follows:

The value of goodwill to be included in the group's statement of financial position in respect of its foreign subsidiary for the year ended 31 December 20X4 is:

AB has taxable temporary differences arising from the revaluation of non current assets.

What is the journal entry to record the movement in the provision for deferred tax resulting from this difference?

The dividend yield of ST has fallen in the year to 31 May 20X5, compared to the previous year.

The share price on 31 May 20X4 was $4.50 and on 31 May 20X5 was $4.00. There were no issues of share capital during the year.

Which of the following should explain the reduction in the dividend yield for the year to 31 May 20X5 compared to the previous year?

RS is a listed entity that has no subsidiaries although its Finance Director is also a director of TU, an unconnected entity.

It is preparing its financial statements to 30 September 20X6.Â

Which of the following substantial transactions must be disclosed in these financial statements in accordance with IAS 24 Related Party Disclosures?

AB acquired a financial investment on 1 January 20X9, incurring $5,000 related agency fees. Â AB initially classified the investment as held for trading, in accordance with IAS 32 Financial Instruments: Presentation.

Which of the following statements reflects the accounting treatment that AB adopted in respect of this investment when it prepared its financial statements to 31 December 20X9?

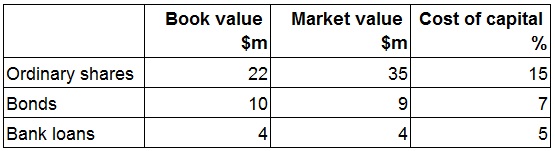

The capital structure of ST is summarised in the table below:

What is the weighted average cost of capital of ST?

Give your answer as a percentage to one decimal place.

? %

If you were asked to express the overall performance of an entity as a percentage of its total investment in net assets which of the following ratios would you calculate?