CIMA F2 - F2 Advanced Financial Reporting

AB sold the majority of its operating equipment to LM for cash on 30 December 20X9 and then immediately leased it back under an operating lease. Â

AB used the cash proceeds from the sale to reduce its long term borrowings significantly. Â No early repayment charge was levied by the lender.

Which of the following statements is true in respect of AB's ratios calculated at 31 December 20X9?

On 1 January 20X8 XY, a listed entity, had 10,000,000 ordinary shares in issue each with a par value of 50 cents. On 1 July 20X8 XY raised $6,000,000 by issuing ordinary shares at a price of £1.50 each which was the full market price.

Place the correct figure into the box below to show the number that XY will use as its weighted average number of ordinary shares in the calculation of earnings per share for the year to 31 December 20X8.

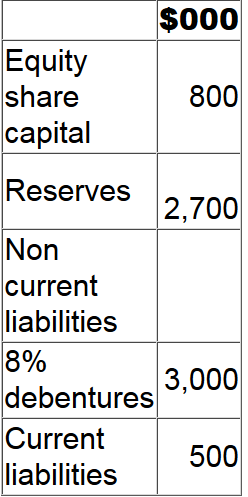

F has profit before interest and tax of $400,000 for the year to 30 June 20X4.

Extracts from F's statement of financial position at 30 June 20X4 are as follows:

Calculate the gearing (debt:equity) ratio at 30 June 20X4.

Give your answer to the nearest whole percentage.

?  %

JK is seeking to raise finance for a project and the directors would prefer to take out a fixed rate bank loan repayable over the next 5 years. The project will increase the profit of JK even after taking into account the additional interest costs.

Which of the following statements about the use of a bank loan in this situation is true?

Information from the financial statements of RST for the year ended 30 April 20X9 is as follows:

Â

At 30 April 20X9 the ordinary shares are trading at $4.75.

What is the price earnings (P/E) ratio for RST at 30 April 20X9?

CD commenced a construction contract on 1 April 20X9. Â The contract value was agreed at $100,000. CD had incurred $40,000 costs to date and estimated costs to completion were $50,000. Â At the year ended 31 December 20X9 this contract was estimated to be 60% complete. Â CD adopted the provisions of IAS 11 Construction Contracts when preparing its financial statements for the year to 31 December 20X9.

What value should be included in CD's profit for the year ended 31 December 20X9 in respect of this contract? Â

Give your answer to the nearest whole number.

$Â ? Â

As at 31 October 20X7 TU's financial statements show the entity having profit after tax of $600,000 and 900,000 $1 ordinary shares in issue. There have been no issues of shares during the year. At 31 October 20X7 TU have 300,000 share options in issue, which allow the holders to purchase ordinary shares at $2 a share in 3 years' time. The average price of the ordinary shares throughout the year was $5 a share.

What is the diluted earnings per share for the year ended 31 October 20X7?

GH is a listed entity which holds equity shares in one subsidiary and one associate.

Information extracted from the most recent financial statements is as follows:

What is the interest cover for the year?

LM and JK operate in the same country and prepare their financial statements to 30 June 20X6 in accordance with International Accounting Standards. On 27 June 20X6 both entities raised $1 million cash by issuing debt instruments with identical terms and conditions. Prior to this issue both entities were financed entirely by equity.

At 30 June 20X6 the gearing ratios, calculated as Debt/Equity x 100%, were as follows:

LM: 30%

JK: 65%

Which of the following independent options would explain the difference between LM and JK's year-end gearing?

A convertible bond with a nominal value of $100 can be redeemed at par in 5 years' time or be converted into 1 new equity share for every $5 of bond held. Â

The current equity share price is $3.50 and it is anticipated that this will grow at a rate of 7% per year.

What is the value of the conversion option of the bond in 5 years' time?

Give your answer to two decimal places.

$Â ? Â