CIMA P1 - Management Accounting

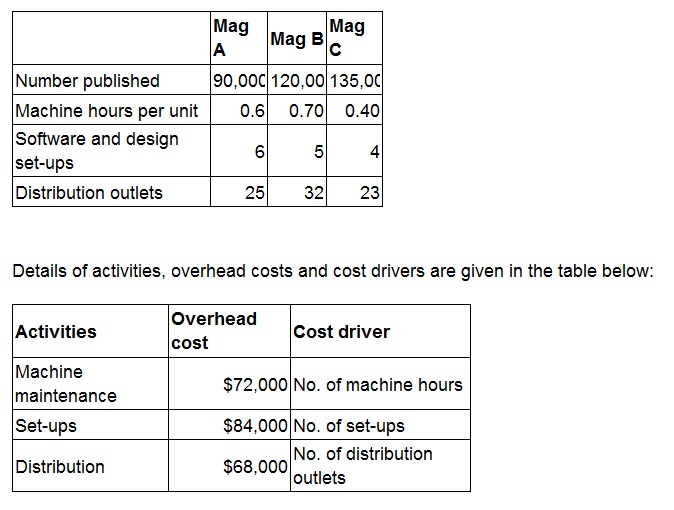

TDM edits, prints and publishes three magazines, Mag A, Mag B and Mag C. The company operates an activity-based costing system.

The following information has been obtained.

What is the overhead cost attributable for each Mag A publication?

Give your answer to the nearest whole cent.

RST is preparing a quotation, on a relevant cost basis, for a special order.

Which TWO of the following are relevant costs that should be included in the quotation?

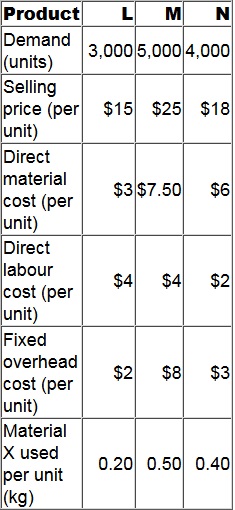

FG Enterprises manufactures and sells three products. There are 4,400 kg of Material X available in the next period. Material X is used in the manufacture of all three products. The following data is available for the next period.

What is the optimal production plan for the next period in order to maximise profit?

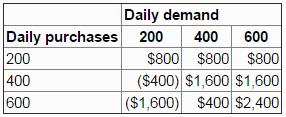

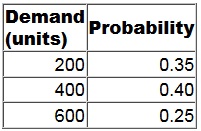

The daily demand for a perishable product has the following probability distribution:

Each unit of the product costs $6 and is sold for $10.

Unsold items are thrown away at the end of the day.

Orders must be placed each morning before the daily demand is known.

The payoff table below shows the profit that would be earned for each of the combinations of purchases and demand.

The number of units that should be purchased at the beginning of each day in order to maximize expected profit is:

You are a trainee management accountant working for a prestigious manufacturing firm. One day you go to a business meeting a business meeting and the managing director is there. They stand up and say that the

company is losing too much money through wastage and losses and so they have decided to implement a total quality management system. They go on to say this system will:

1:Allow the company to improve on a consistent and continual basis

2:Allow the company to identify and allocate quality accountability to certain departments

3:Help the company detect error and fraud

Are ALL of these statements correct?

A manufacturing company has fixed production overhead costs, direct material costs and direct labour costs. The number of units of closing finished goods inventory is lower than the opening inventory.

Which of the following statements is true?

A company develops computer software programs to meet each client's specific requirements. The management accountant is considering introducing a standard costing system.

Which THREE of the following are reasons that support the case for the company's introduction of a standard costing system?

CDF is a manufacturing company within the DF group. CDF has been asked to provide a quotation for a contract for a new customer and is aware that this could lead to further orders. As a consequence, CDF will produce the quotation by using relevant costing instead of its usual method of full cost plus pricing. The following information has been obtained in relation to the contract: Material D 40 tons of material D would be required. This material is in regular use by CDF and has a current purchase price of $38 per ton. Currently, there are 5 tons in inventory which cost $35 per ton. The resale value of the material in inventory is $24 per ton.

Components 4,000 components would be required. These could be bought externally for $15 each or alternatively they could be supplied by RDF, another company within the DF manufacturing group. The variable cost of the component if it were manufactured by RDF would be $8 per unit, and RDF adds 30% to its variable cost to contribute to its fixed costs plus a further 20% to this total cost in order to set its internal transfer price. RDF has sufficient capacity to produce 2,500 components without affecting its ability to satisfy its own external customers. However, in order to make the extra 1,500 components required by CDF, RDF would have to forgo other external sales of $50,000 which have a contribution to sales ratio of 40%.

Labour hours 850 direct labour hours would be required. All direct labour within CDF is paid on an hourly basis with no guaranteed wage agreement. The grade of labour required is currently paid $10 per hour, but department W is already working at 100% capacity. Possible ways of overcoming this problem are: • Use workers in department Z, because it has sufficient capacity. These workers are paid $15 per hour. • Arrange for sub-contract workers to undertake some of the other work that is performed in department W. The sub-contract workers would cost $13 per hour.

Specialist machine The contract would require a specialist machine. The machine could be hired for $15,000 or it could be bought for $50,000. At the end of the contract if the machine were bought, it could be sold for $30,000. Alternatively, it could be modified at a cost of $5,000 and then used on other contracts instead of buying another essential machine that would cost $45,000. The operating costs of the machine are payable by CDF whether it hires or buys the machine. These costs would total $12,000 in respect of the new contract.

Supervisor The contract would be supervised by an existing manager who is paid an annual salary of $50,000 and has sufficient capacity to carry out this supervision. The manager would receive a bonus of $500 for the additional work.

Development time 15 hours of development time at a cost of $3,000 have already been worked in determining the resource requirements of the contract.

Fixed overhead absorption rate CDF uses an absorption rate of $20 per direct labour hour to recover its general fixed overhead costs. This includes $5 per hour for depreciation.

Calculate the relevant cost of the contract to CDF. You must present your answer in a schedule that clearly shows the relevant cost value for each of the items identified above. You should also explain each relevant cost value you have included in your schedule and why any values you have excluded are not relevant.

Ignore taxation and the time value of money.

Select all the true statements.

Which of the following statements regarding marginal and absorption costing are true in the context of pricing decisions?

Select ALL that apply.

The labour requirement for a special contract is 250 skilled labour hours paid at $10 per hour and 750 semi-skilled labour hours paid at $8 per hour.

At present, skilled labour is fully utilised on other contracts which generate a $12 contribution per hour, after charging labour costs. Additional skilled labour is unavailable in the short term.

There is a surplus of 1,200 semi-skilled hours over the period of the contract but the firm has a policy of no redundancies.

The relevant cost of labour for the special contract is: