CIMA P1 - Management Accounting

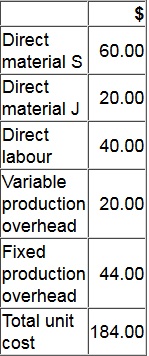

The cost card for one unit of Product G is as follows:

The opening and closing inventories of Product G for month 5 are budgeted to be 10 units and 60 units respectively.

Profit for month 5 using absorption costing is budgeted to be $15,000.

What is the budgeted profit for month 5 using throughput costing?

A company manufactures headphones.

70% of production costs are prime costs. Production overhead costs are driven by the number of headphones produced.

Which costing system would be most appropriate for product profitablilty analysis?

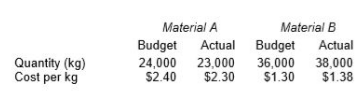

A company produces a product that requires two materials, Material A and Material B. Details of the material quantities and costs for August are given in the table below.

Budgeted and actual output of the product for August was 12,000 units.

The material mix variance for August is:

A snowboard manufacturer is considering investing in technology that will give a good indication of how heavy snowfall will be in the future. The predictions tend to be reasonably accurate.

The current budgeted profit for the year is £2,560,000 but if they invest in this technology and it works, the expected profit will be £2,640,000. The manufacturer is willing to invest a maximum of £40,000 into the venture.

What is the expected profit if the investment is NOT made?

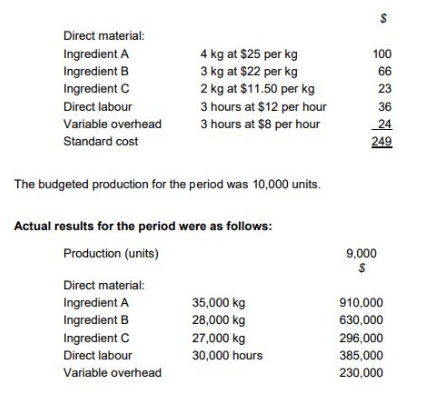

TP makes wedding cakes that are sold to specialist retail outlets which decorate the cakes according to the customers’ specific requirements. The standard cost per unit of its most popular cake is as follows:

The general market prices at the time of purchase for Ingredient A and Ingredient B were $23 per kg and $20 per kg respectively. TP operates a JIT purchasing system for ingredients and a JIT production system; therefore, there was no inventory during the period.

What was the material price planning variance for ingredient B?

Which of the following, regarding costing methods, is true?

Which THREE of the following would be contained within a master budget?

The term ‘budgetary slack’ refers to the:

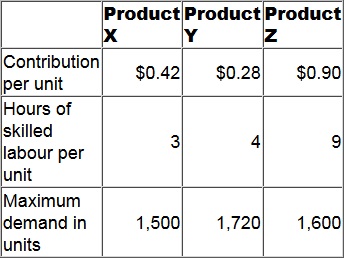

A company has only 10,100 hours of skilled labour available next period.

Data for its three products for next period are as follows.

At least 500 units of each product must be sold each period.

No inventories are held.

How many units of Product X should be manufactured next period in order to maximise profit?

For the forthcoming period, the number of units of product L produced must be no more than four times the number of units of product M produced.

The equation to represent this constraint in a linear programming exercise is: