CIMA P1 - Management Accounting

A company has budgeted to produce 5,000 units of Product B per month. The opening and closing inventories of Product B for next month are budgeted to be 400 units and 900 units respectively. The budgeted selling price and variable production costs per unit for Product B are as follows:

Total budgeted fixed production overheads are $29,500 per month.

The company absorbs fixed production overheads on the basis of the budgeted number of units produced. The budgeted profit for Product B for next month, using absorption costing, is $20,700.

Prepare a marginal costing statement which shows the budgeted profit for Product B for next month.Â

What was the marginal costing profit for the next month?

A company's initial budget for month 3 includes sales of $100,000, a contribution to sales (C/S) ratio of 40% and fixed costs of $20,000.

If the budgeted sales volume in month 3 is reduced by 5% but contribution per unit, total fixed costs and sales mix are unchanged, which of the following statements, about the change to the budgeted profit or contribution in month 3 is true?

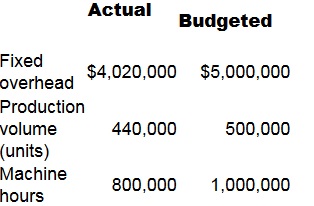

Company Y absorbs fixed production overheads using a rate per machine hour. Budgeted and actual data for month 8 are as follows:

What is the fixed production overhead efficiency variance?

A medium-sized manufacturing company, which operates in the electronics industry, has employed a firm of consultants to carry out a review of the company’s planning and control systems. The company presently uses a traditional incremental budgeting system and the inventory management system is based on economic order quantities (EOQ) and reorder levels. The company’s normal production patterns have changed significantly over the previous few years as a result of increasing demand for customized products. This has resulted in shorter production runs and difficulties with production and resource planning.

The consultants have recommended the implementation of activity based budgeting and a manufacturing resource planning system to improve planning and resource management.

Select ALL the benefits for the company that could occur following the introduction of an activity based budgeting system.

XY, a not-for-profit charity organization which is funded by public donations, is concerned that it is not making the best use of its available funds. It has carried out a review of its budgeting system and is considering replacing the current system with a zero-based budgeting system.

Select ALL the potential advantages AND disadvantages for the charity of a zero-based budgeting system.

Where sales volume is the principal budget factor, which of the following is the correct order in which budgets have to be prepared?

Which THREE of the following are never relevant costs for short-term decision making?

A manager has not yet used all oh his budget. He is worried that his budget maybe reduced next year if he is not seen to have needed all the funds. He decides to spend the remaining £1,580 on another team building

exercise as well as a catered lunch for his department.

This example falls under which behavioural aspect of budgetary control?

A master budget comprises which of the following?

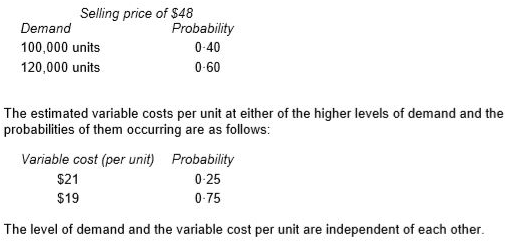

PL currently earns an annual contribution of $2,880,000 from the sale of 90,000 units of product B. Fixed costs are $800,000 per annum.

The management of PL is considering reducing the selling price per unit to $48. The estimated levels of demand at the revised selling price and the probabilities of them occurring are as follows:

Calculate the probability that the profit will increase from its current level if the selling price is reduced to $48.