CIMA P1 - Management Accounting

A company uses limiting factor analysis to identify its optimal production plan. All of the company's products are manufactured in house and cannot be bought in.

What objective is assumed with limited factor analysis?

LM operates a parcel delivery service. Last year its employees delivered 15,120 parcels and travelled 120,960 kilometers. Total costs were $194,400.

LM has estimated that 70% of its total costs are variable with activity and that 60% of these costs vary with the number of parcels and the remainder vary with the distance travelled.

LM is preparing its budget for the forthcoming year using an incremental budgeting approach and has produced the following estimates:

• All costs will be 3% higher than the previous year due to inflation

• Efficiency will remain unchanged

• A total of 18,360 parcels will be delivered and 128,800 kilometers will be travelled.

Calculate the following costs to be included in the forthcoming year’s budget:Â

(i) the total variable costs related to the number of parcels delivered.Â

(ii) the total variable costs related to the distance travelled.

Which one of the following would NOT be included in a decision to close a division of an organization?

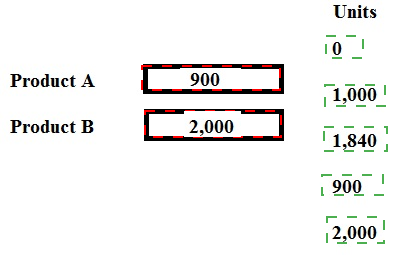

Demand for two products, A and B is 1,000 units and 2,000 units respectively. Each unit of Product A requires 8 kg of material and each unit of Product B requires 5 kg of material. The maximum availability of material is 17,200 kg. Contribution per unit of A is $10 and per unit of B is $9.

Place the production volumes of Product A and Product B, that will maximize contribution, in the table.

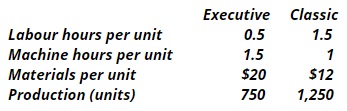

D3 makes 2 types of toilets - the Executive (Ex) and the Classic (CI). Direct labour costs $6 per hr and overheads are absorbed on a machine hour basis. The overhead absorption rate for the period is $28 per machine hour. What is the traditional cost per unit for (Ex) and (CI)?

Sales volumes reported for the latest period are used by managers as the basis to forecast sales for the forthcoming period. The forecasts are compared with the budgeted sales and plans are adjusted to ensure that the budgeted sales are achieved.

This is an example of:

A company has identified the trend in its sales figures through the regression equation Y = 65.9 + 3.86X, where Y is the sales revenue in thousands of dollars and X is the month number. The average seasonal variation for October is 87%

Calculate the forecast sales revenue for October of Year 6.

Give your answer to the nearest $000.

8fb9be1c-b0d5-4acb-8cfb-f4b4426e641B. The primary objective of Company A is to maximise profit. It is now deciding on the optimum production mix for the next period and has one limited production resource.

The production mix decision should be based on: