CIMA P1 - Management Accounting

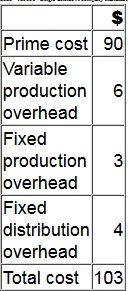

A company manufactures a single product. The cost card for a unit of this product is as follows:

During month 6, finished goods inventory increased by 350 units.

By how much would the profit differ in month 6 if finished goods inventory was valued at standard marginal cost rather than standard absorption cost?

A company currently uses a rate of $32 per machine hour to absorb its total production overheads of $960,000.

Using this system the production overhead cost per unit of product X is $160.

An activity based costing exercise has revealed that only $345,000 of the production overhead is driven by machine hours. The remainder is driven by the number of machine set ups, at a rate of $9.60 per set up.

Product X requires 3 set ups per unit.

Calculate the total production overhead cost per unit of product X using an activity based costing system.

Give your answer to two decimal places.

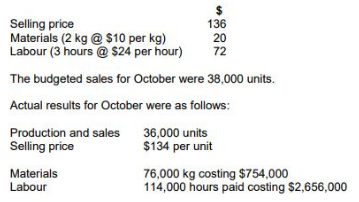

GH manufactures a product using skilled labour and high quality materials. The company operates a standard costing system and a just-in-time (JIT) purchasing and production system. The standard selling price and variable costs for one unit of the product are as follows:

Prepare a statement that reconciles the budgeted contribution with the actual contribution for October. Your statement should show the variances in as much detail as possible.

What was the actual contribution for October?

Which TWO of the following statements are true for obtaining a reliable forecast from a time series?

‘A zero-based budgeting system involves establishing decision packages that are then ranked in order of their relative importance in meeting the organization’s objectives’.Â

Which of the following is true regarding he difficulties that a not-for-profit organization may experience when trying to rank decision packages.

Select ALL true statements.

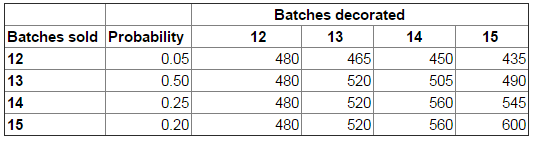

A bakery manager is deciding how many batches of birthday cakes to decorate each day.

Demand for the birthday cakes varies from 12 to 15 batches per day. Each batch decorated and sold earns a contribution of $40 but each batch unsold leads to loss of contribution of $15.

The payoff table below shows the total $ contribution from each of the possibilities:

Based on expected values, the number of batches of birthday cakes the bakery manager should decorate each day is:

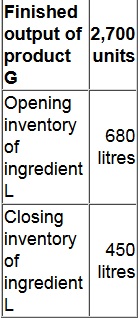

Each finished unit of product G contains 2 litres of ingredient L. Losses during production are 10% of input of ingredient L. Budgeted data for next period are as follows:

The budgeted purchases of ingredient L for next period are:

Which of the following would help to explain a favourable material price variance?

Explain why sensitivity analysis is useful when dealing with uncertainty in project

appraisal.

Select all the true statements.

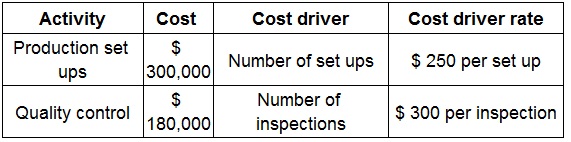

XY manufactures a range of products and uses an activity based costing system.

Budgeted production of Product B is 7,500 units.

Overheads have been identified by activity and related to appropriate cost drivers.

Product B is produced in batches of 250 units. Machines have to be reset after every batch and quality inspections are carried out on every third batch.

What is the total overhead cost per unit of Product B?

Give your answer to two decimal places.