CIMA BA2 - Fundamentals of management accounting

A company operates an absorption costing system. Overheads are absorbed using a pre-determined absorption rate using labour hours.

Actual labour hours were 10% below budget for the period and overheads incurred were 10% above budget for the period. This would result in:

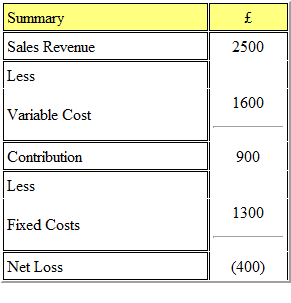

Refer to the exhibit.

An income statement summary for a particular product shows the following:

In which of the following circumstances would it be appropriate to continue to produce the product?

In investment appraisal, the internal rate of return is

C Ltd produces a chemical in a single process. Information for this process last month is as follows:

(a) Opening work in progress - 10000 kg valued at £10000 for direct material and £7500 for conversion costs.

(b) Materials input - 25000 kg at £1.10 per kg.

(c) Conversion costs - £17000

(d) Output during the month - 23000 kg.

(e) There were 7500 units of closing work in progress which was complete as to materials and 30% complete as to conversion.

(f) Normal loss for the month was 10% of input and all losses have a scrap value of 80p per kg.

What was the average cost per kg of finished output during the month?

Which of the following is the LEAST appropriate basis on which to apportion the insurance costs of plant and machinery:

Which of the following industries would not use process costing?

Apex Plc has budgeted to sell 8,000 units of A in the year. Opening inventory of A is estimated at 1,000 units and the company plans to reduce inventory levels of all products by 15%.

What will be the production budget (in units) for the year?

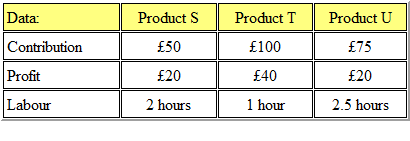

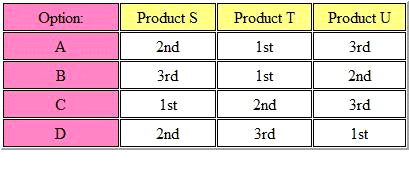

Refer to the exhibit.

C Ltd manufactures three products, which require the same type of materials. The following contribution and profit per unit is available:

In a period in which labour hours are in short supply, which of the following options is the rank order of production?

An increase in the variable cost per unit, will cause the point at which the line plotted on a profit/volume (PV) graph intersects the horizontal axis to:

Each finished carton of product P contains 15 litres of liquid L. During the production process there is an unavoidable loss of 20% of the liquid input. The standard price of liquid L is $2 per litre.

The standard ingredient cost for liquid L shown on the standard cost card for one carton of product P will be