CIMA BA2 - Fundamentals of management accounting

A company operates a full cost system of pricing. Production overheads are absorbed using a pre-determined absorption rate of £3.50 per machine hour. The direct production cost of product A is £15 per unit and it utilises 6 machine hours per unit. The mark-up for non-production costs is 10% of total production cost. The company wants to make a 25% return on sales revenue for all products.

The required selling price for Product A, to two decimal places, is:

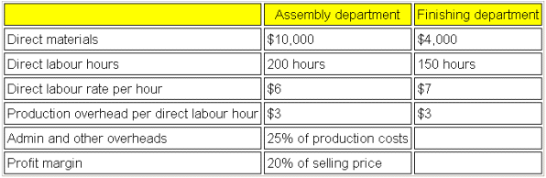

Refer to the exhibit.

The following information relates to Job 123:

The selling price to the customer for Job 123 is:

Which one of the following is a characteristic of strategic financial information?

The accounting treatment for overheads over absorbed is to:

An overtime premium may be defined as:

The following costs are incurred by a company which owns a five star hotel. Which THREE of the items would normally be classified as variable costs?

The principal budget factor can be defined as:

The standard labour cost for 1 component is $15.00 (5 hours at $3 per hour). Last month, 6,000 hours were worked at a cost of $17,000 to produce 1,100 components. The labour efficiency variance was:

A company’s cash budgetary plans show that there will be surplus cash for three months of the forthcoming year.

Which THREE of the following would be appropriate management actions in this situation?

The wages of a machine operator who is paid a guaranteed minimum wage plus a bonus for each unit produced would be described as A.